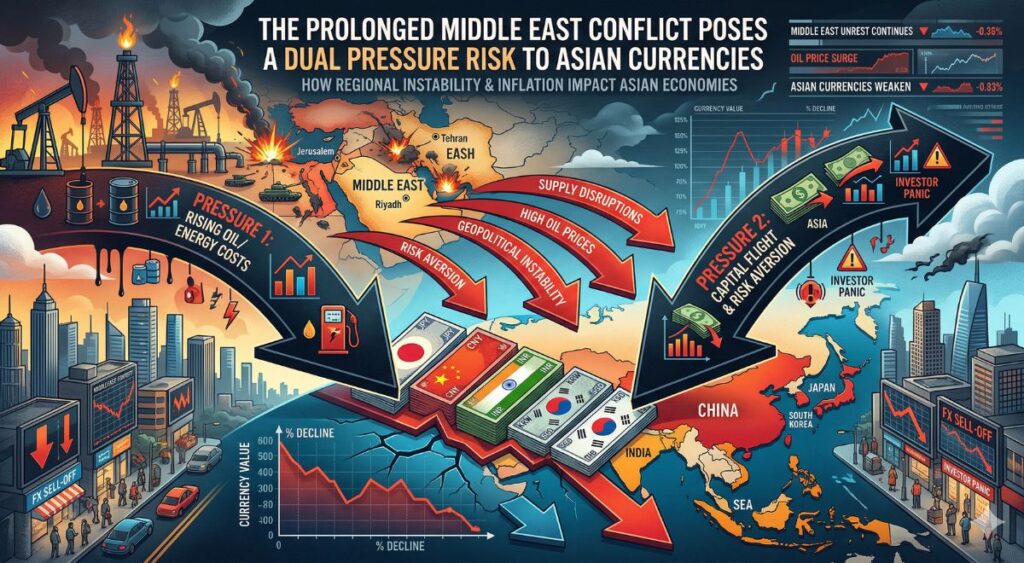

The ongoing conflict in the Middle East is no longer a regional concern—it is steadily evolving into a global economic risk with far-reaching implications. Among the most vulnerable are Asian currencies, which are facing a dual pressure threat stemming from rising energy costs and increasing financial market uncertainty.

Energy Shock: A Direct Hit to Import-Dependent Economies

Asia is heavily reliant on energy imports, particularly crude oil and natural gas from the Middle East. As geopolitical tensions persist, the risk of supply disruptions has pushed global oil prices higher. This presents a major challenge for countries like India, Japan, South Korea, and Pakistan, all of which depend significantly on imported fuel.

Higher oil prices widen trade deficits, increase inflation, and weaken local currencies. When countries spend more on energy imports, demand for the U.S. dollar rises—putting downward pressure on domestic currencies such as the Indian rupee, Japanese yen, and Pakistani rupee.

For emerging Asian economies already dealing with fragile external balances, this creates a dangerous cycle: rising import costs → widening deficits → currency depreciation → further inflation.

Safe-Haven Demand: Capital Flows Shift Away from Asia

The second layer of pressure comes from global financial markets. During times of geopolitical uncertainty, investors typically move their capital into “safe-haven” assets such as the U.S. dollar, gold, and U.S. Treasury bonds.

This shift in investor sentiment leads to capital outflows from emerging Asian markets, further weakening their currencies. As foreign investors pull money out of equities and bonds, demand for local currencies falls, accelerating depreciation.

Currencies like the Indonesian rupiah, Thai baht, and Philippine peso are particularly sensitive to such capital movements, making them vulnerable during prolonged geopolitical crises.

Central Banks Caught in a Policy Dilemma

Asian central banks now face a difficult balancing act. To stabilize their currencies, they may need to raise interest rates or intervene in foreign exchange markets. However, tighter monetary policy can slow economic growth—especially in countries still recovering from previous global shocks.

For policymakers, the challenge is clear: defend the currency without derailing economic recovery.

Trade and Supply Chain Disruptions Add to the Strain

Beyond energy and capital flows, the conflict also threatens key global shipping routes. Any disruption in critical chokepoints—such as the Strait of Hormuz or the Red Sea—can delay shipments, increase freight costs, and further strain Asian export-driven economies.

This compounds the pressure on currencies by weakening trade performance and reducing foreign exchange earnings.

Outlook: Volatility Likely to Persist

As long as tensions in the Middle East remain unresolved, Asian currencies are expected to remain volatile. The combination of elevated oil prices and cautious investor sentiment creates a challenging environment for both emerging and developed economies in the region.

While some countries with strong foreign reserves may be better equipped to manage the shock, others could face prolonged currency weakness and inflationary pressures.